http://fwd5.wistia.com/medias/18wxl2n43f?embedType=iframe&videoFoam=true&videoWidth=640

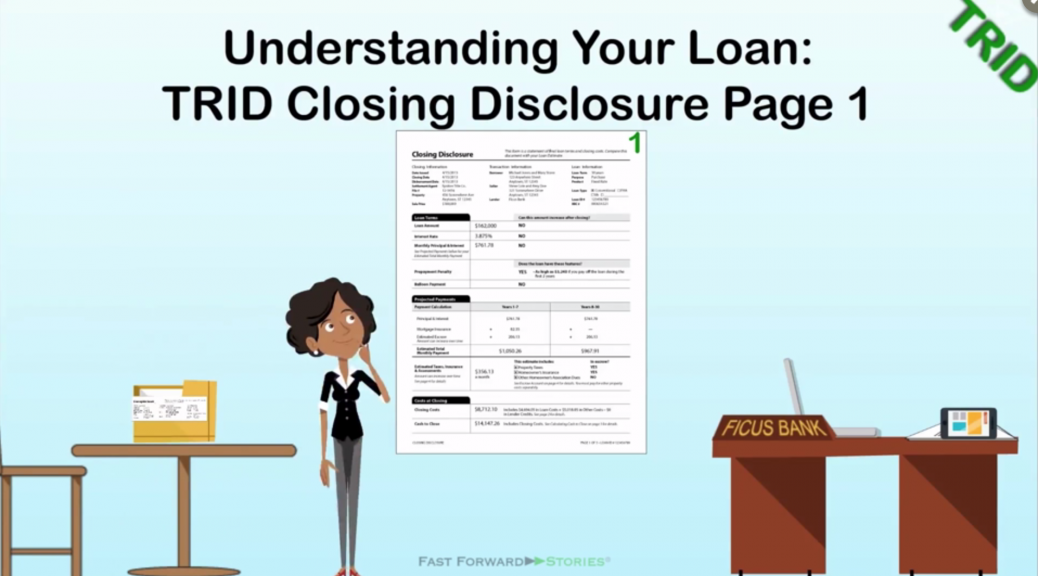

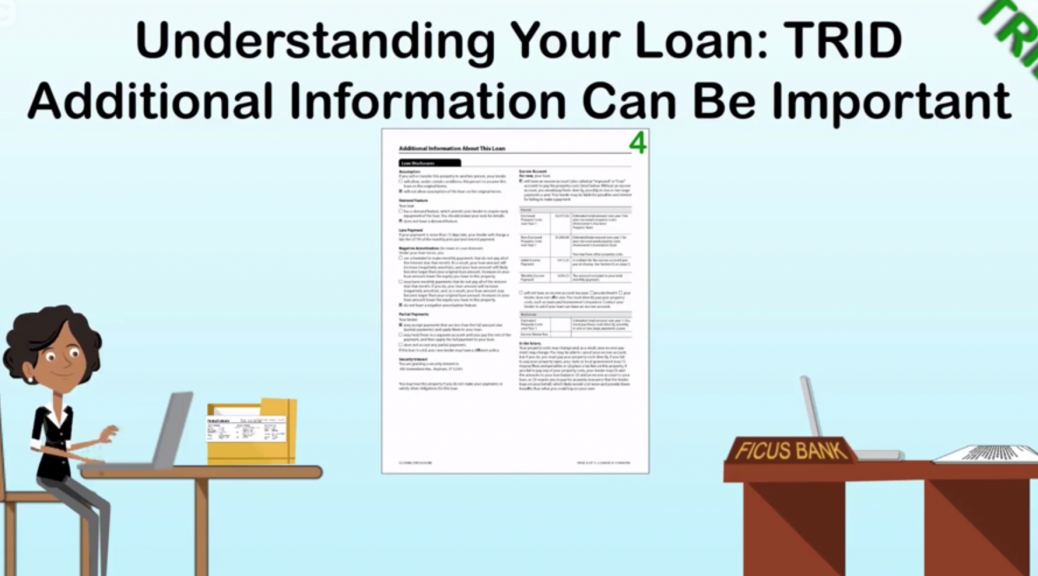

Page 4 of your Closing Disclosure is important. It is NOT just standardized form information that is identical for every loan.

Review these terms:

- Assumption: can this loan be transferred to another person if you sell or transfer the property?

- Demand: can the lender require early repayment of the loan?

- Late Payments: what penalty, after what period, applies?

- Negative Amortization: does this loan schedule or allow payments that do NOT fully cover the interest due, resulting in increased loan principal?

- Partial Payments: what is THIS lender’s policy?

You should also review Escrow Account details to understand whether you will pay additional property costs via regular Escrow Account payments or handle them yourself directly.