http://fwd5.wistia.com/medias/6tzbc4922p?embedType=iframe&videoFoam=true&videoWidth=640 These costs are paid to outside parties, not the lender, but you don’t get to choose them. They may include: appraisal, which puts a value on your property on Read More

http://fwd5.wistia.com/medias/49we28kmt9?embedType=iframe&videoFoam=true&videoWidth=640 Closing costs are fees paid when the title of the property is transferred to the buyer making them the legal owner. Origination Charges are fees collected by the lender Read More

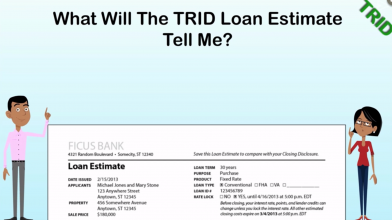

http://fwd5.wistia.com/medias/i9fota2dpy?embedType=iframe&videoFoam=true&videoWidth=640 The first page of your Loan Disclosure shows the Loan Terms Projected Payments and Costs at Closing. The Loan Amount, of course is the total you are borrowing. But Read More

http://fwd5.wistia.com/medias/u50xeawkix?embedType=iframe&videoFoam=true&videoWidth=640 If an eligible loan proceeds from Estimate to closing, creditors must provide a Closing Disclosure form documenting the actual transaction terms and costs THREE business days before consummation. It Read More

http://fwd5.wistia.com/medias/stlcehm7qu?embedType=iframe&videoFoam=true&videoWidth=640 Yes, if circumstances change, such as: a natural disaster damages the property or affects closing costs the title insurer providing the estimate goes out of business during underwriting new Read More

http://fwd5.wistia.com/medias/0k5k9nuvuy?embedType=iframe&videoFoam=true&videoWidth=640 Creditors are generally bound by the initial Loan Estimate. They are permitted to provide a revised Loan Estimate only under certain changed circumstances. These include circumstances that: a) increase Read More

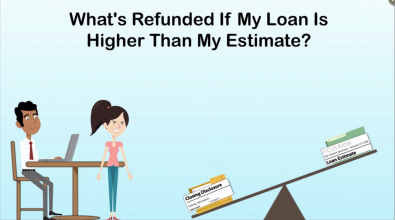

http://fwd5.wistia.com/medias/jc5jmcwox5?embedType=iframe&videoFoam=true&videoWidth=640 If the amount you pay at closing exceeds the amounts disclosed on the Loan Estimate – beyond tolerance limits for each category – the creditor must REFUND the excess Read More

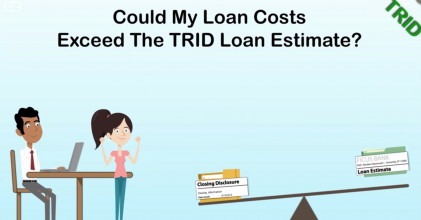

http://fwd5.wistia.com/medias/bzr9ba7ahr?embedType=iframe&videoFoam=true&videoWidth=640 Yes, within defined limits. Service charges for which YOU shop and select a provider may change; the creditor is NOT responsible for providers who are NOT on their written Read More

http://fwd5.wistia.com/medias/lm1qq356su?embedType=iframe&videoFoam=true&videoWidth=640 The Loan Estimate documents the essential facts and terms of an approved real estate loan. It includes: loan terms projected payments and loan costs cash and costs at closing Read More

http://fwd5.wistia.com/medias/hxthum9hb1?embedType=iframe&videoFoam=true&videoWidth=640 Under the TRID rule, creditors must retain Escrow Cancellation and Partial Payment Policy disclosures for two years; Loan Estimate records for three years after loan consummation and Closing Disclosures Read More