http://fwd5.wistia.com/medias/rzowf54ev8?embedType=iframe&videoFoam=true&videoWidth=640

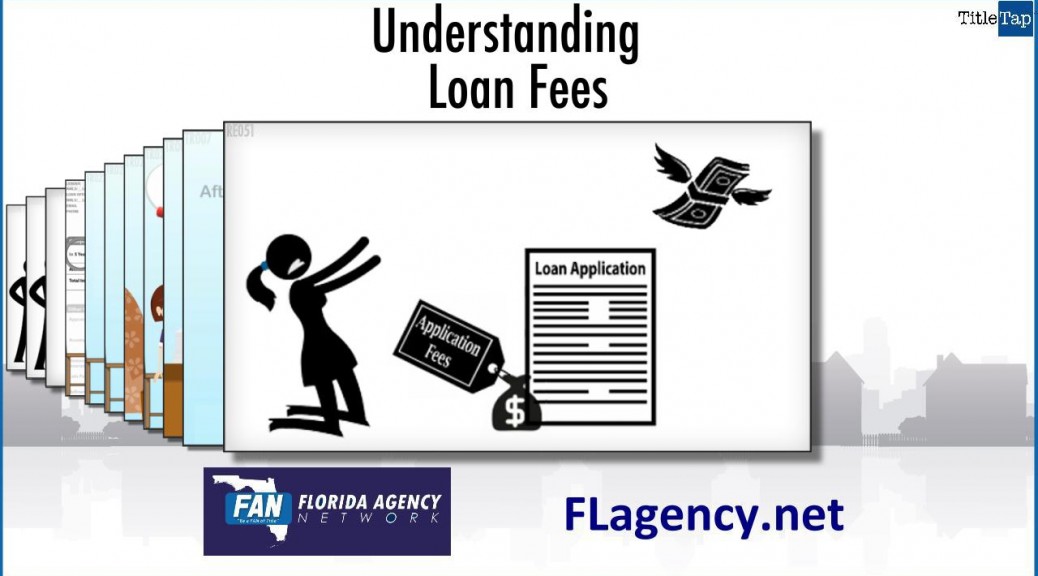

Yes, loan origination involves costs and fees. As you’ll see in the video, when you turn in your application you’ll be required to pay a loan application fee to cover the costs of underwriting the loan. This fee pays for the home appraisal a copy of your credit report and any additional charges that may be necessary.

The application fee is generally non-refundable.