Here’s a full timeline of how we created the Loan Estimate and Closing Disclosure forms, part of our Know Before You Owe: Mortgages project. It’s a look back at our effort to make mortgage disclosures simpler and more effective, with the input of the people who will actually use them.

July 21, 2010

The Dodd-Frank Wall Street Reform and Consumer Protection Act is signed into law.

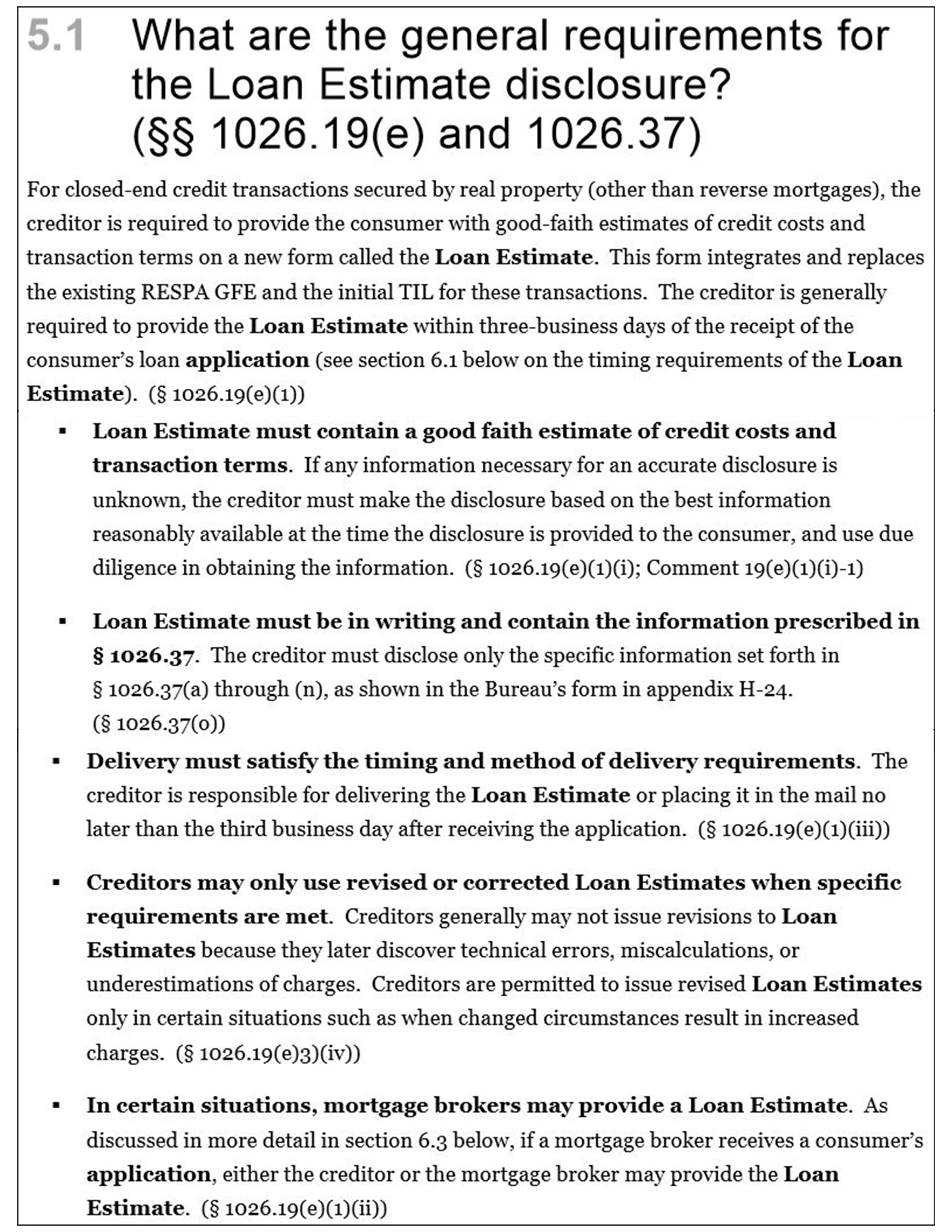

The new law required the CFPB to combine the Truth in Lending and Real Estate Settlement Procedures Act disclosures.

December 6, 2010

The Treasury Department hosts a mortgage disclosure symposium.

The event brought together consumer advocates, industry, marketers, and more to discuss CFPB implementation of the combined disclosures.

February 21, 2011

Design begins.

Starting with the legal requirements and the consumer in mind, we began sketching prototype forms for testing.

During this process, the team discussed preliminary issues and ideas about mortgage disclosures. This session set the context for the disclosures and was a starting point for their development. The team continued to develop these issues and ideas over more than a year during the development process.

May 18, 2011

Know Before You Owe opens online.

We posted the first two prototype loan estimates. We asked consumers and industry to examine them and tell us what worked and what didn’t. We repeated this process for several future rounds. Over the course of the next ten months, people submitted more than 27,000 comments.

May 19, 2011 – May 24, 2011

Qualitative testing begins in Baltimore.

We sat down with consumers, lenders, and brokers to examine the first set of loan estimate prototypes to test two different graphic design approaches.

Disclosures tested:

Prototype A

Prototype B

June 27, 2011 – July 1, 2011

Los Angeles, CA

Consumers and industry participants worked with prototypes with lump sum closing costs and prototypes with itemized closing costs.

Disclosures tested:

Prototype A

Prototype B

August 1, 2011 – August 3, 2011

Chicago, IL

Again, we asked testing participants to work with prototypes with lump sum closing costs and itemized closing costs.

Disclosures tested:

Prototype A

Prototype B

September 12, 2011 – September 14, 2011

Springfield, MA

Another round of closing cost tests, as we presented participants with one disclosure that had the two-column design from previous rounds and another that used new graphic presentations of the costs.

Disclosures tested:

Prototype A

Prototype B

October 17, 2011 – October 19, 2011

Albuquerque, NM

In this round, we presented closing costs in the itemized format and worked on a table that shows how payments change over time.

Disclosures tested:

Prototype A

Prototype B

November 8, 2011 – November 10, 2011

Des Moines, IA

We began testing closing disclosures. Both designs included HUD-1-style numbering for closing details, but two different ways of presenting other costs and Truth in Lending information.

Disclosures tested:

Prototype A

Prototype B

December 13, 2011 – December 15, 2011

Birmingham, AL

One form continued to use the HUD-1 style numbered closing cost details; the other was formatted more like the Loan Estimate, carrying over the Cash to Close table and no line numbers.

Disclosures tested:

Prototype A

Prototype B

January 24, 2012 – January 26, 2012

Philadelphia, PA

In this round, we settled on prototypes formatted like the Loan Estimate, but one included line numbers and the other didn’t. We also began testing the Loan Estimate with the Closing Disclosure.

Disclosures tested:

Prototype A

Prototype B

Prototype C

February 20, 2012 – February 23, 2012

Austin, TX

Participants reviewed one Loan Estimate and one Closing Disclosure (with line numbers) to see how well they worked together.

Disclosures tested:

Prototype A

Prototype B

February 21, 2012

We convene a small business review panel.

A panel of representatives from the CFPB, the Small Business Administration (SBA), and the Office of Management and Budget (OMB) considered the potential impact of the proposals under consideration on small businesses that will provide the mortgage disclosures.

March 6, 2012

We meet with small businesses.

The panel met with small businesses and asked for their feedback on the impacts of various proposals the CFPB is considering. This feedback is summarized in the panel’s report.

(Note: Link to large PDF file.)

March 26, 2012

Back to Baltimore!

We conducted one final round of testing to confirm that some modifications from the last round work for consumers.

Disclosures tested:

Prototype A

Prototype B

Prototype C

July 9, 2012

Proposal of the new rule.

The CFPB released a Notice of Proposed Rulemaking. The notice proposed a new rule to implement the combined mortgage disclosures and requested your comments on the proposal.

November 6, 2012

Comment period on most of the proposed rule closes.

Between the public comment period and other information for the record, the CFPB reviewed nearly 3,000 comments. These comments helped us improve the disclosures and the final rule.

October 11, 2012 – December 13, 2012

We test Spanish language versions of the disclosures across the country.

We conducted qualitative consumer testing on Spanish language versions of the proposed disclosures. We tested in three cities: Arlington, Va. (October 11-12); Phoenix, Az. (November 14-15); and Miami, Fla. (December 12-13).

April 23, 2013 – June 13, 2013

Validating our testing

With the help of Kleimann Communication Group, the contractor who helped us throughout the testing process, we conducted a quantitative study of the new forms with 858 consumers in 20 locations across the country. By nearly every measure, the study showed that the new forms offer a statistically significant improvement over the existing forms.

June 18, 2013 – July 26, 2013

Additional testing with modified disclosures

In response to comments, we developed and tested different versions of the disclosures for refinance loans, which we tested for three rounds. (In our last round, we tested a modification for both purchases and refinances.) We also did one more round of Spanish language testing for the refinance versions. The modified disclosures tested well and are the ones included in the final rule.

November 20, 2013

A final rule

The CFPB issues a Final Rule. The final rule creates new integrated mortgage disclosures and details the requirements for using them. The rule is effective for mortgage applications received starting August 1, 2015.

June 24, 2015

New Effective Date Proposed

The CFPB proposes a new effective date of October 3, 2015 for the Know Before You Owe mortgage disclosure rule.

July 21, 2015

New Effective Date Announced

The CFPB issues a final rule moving the effective date to October 3, 2015.