http://fwd5.wistia.com/medias/4vq1aq79x6?embedType=iframe&videoFoam=true&videoWidth=640

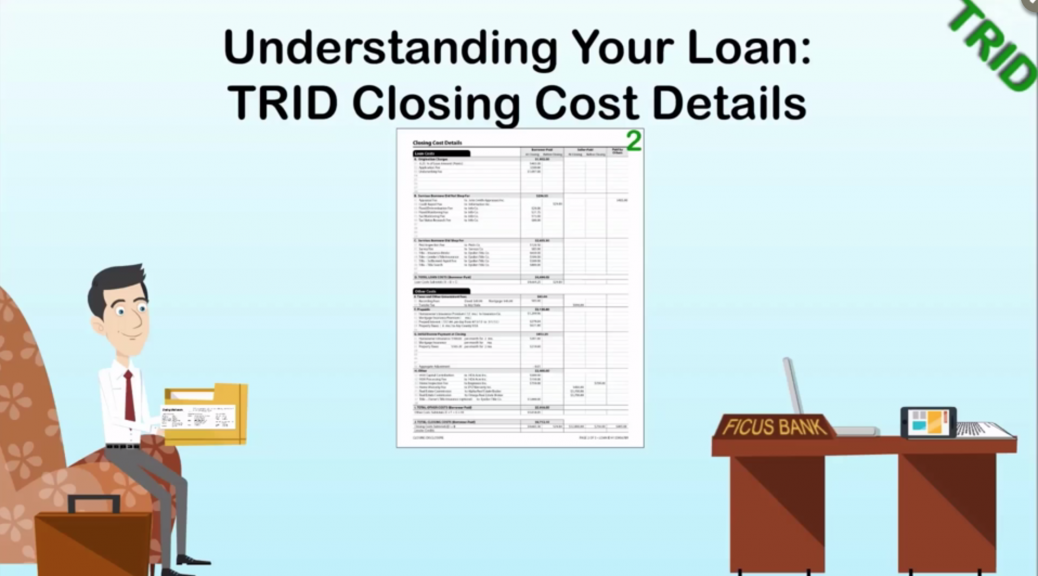

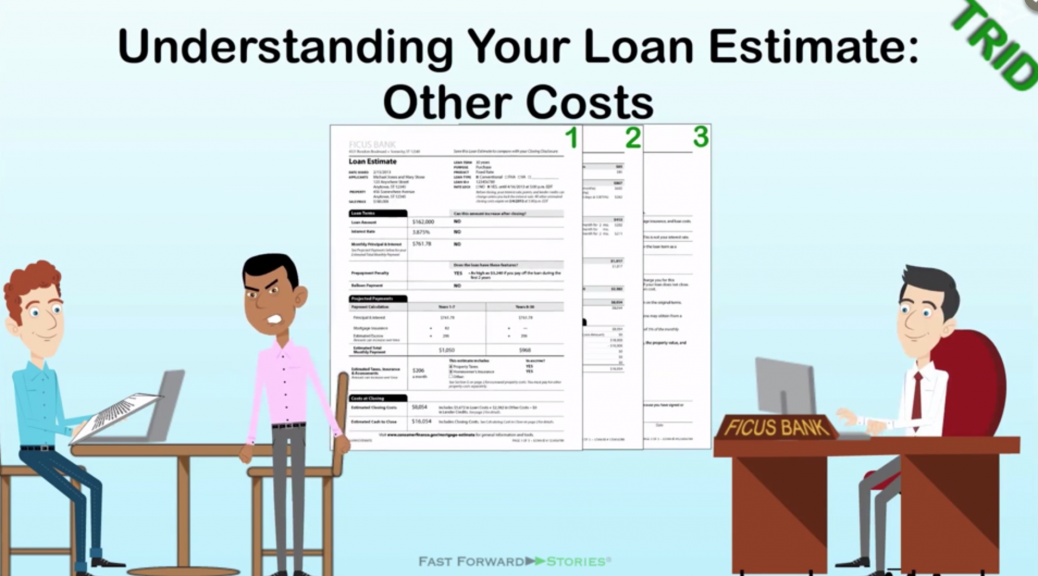

Real estate transactions require taxes, certain pre-payments, and escrow funding.

Recording fees are charged by government agencies for keeping legal ownership records, while “transfer taxes” may be imposed by states, counties and municipalities on real estate ownership transfers.

Prepayments may include homeowner’s insurance premiums on the property mortgage insurance, if required property taxes for a period of months in advance, and prepaid interest, typically for the period from closing to the first mortgage payment.

Escrow funding may also be required against future annual charges for homeowners insurance, mortgage insurance and property taxes.

Title insurance on YOUR legal ownership – “Owner’s Title Policy” – may be designated as optional, which only indicates that it is not required by this creditor.

Some of these “Other Costs” may vary substantially between Loan Estimate and Closing Disclosure ask your lender about the tolerance rules or watch the video “Could My Loan Cost Exceed The Loan Estimate?”