http://fwd5.wistia.com/medias/z3e7qpi1df?embedType=iframe&videoFoam=true&videoWidth=640

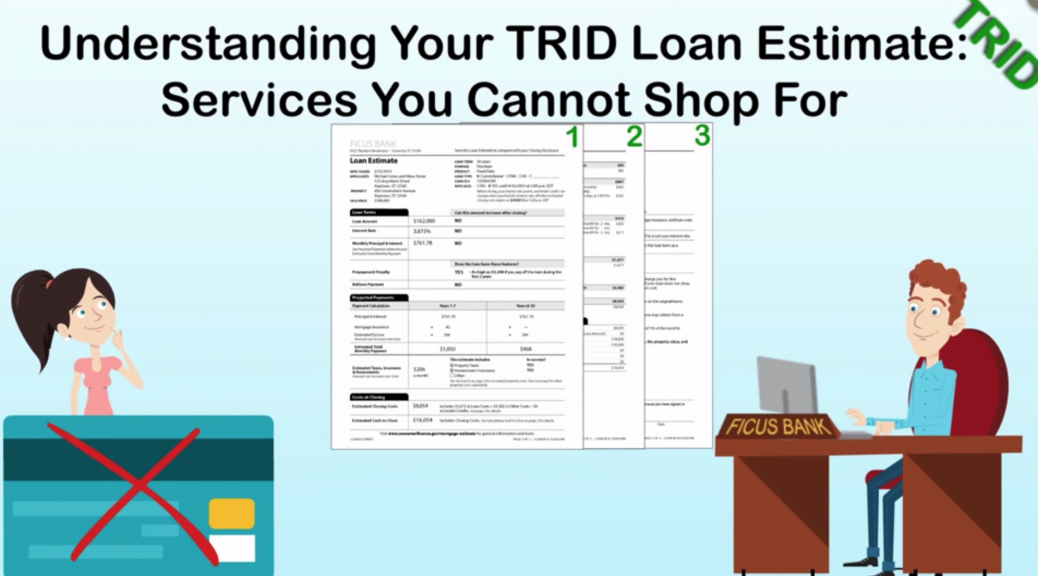

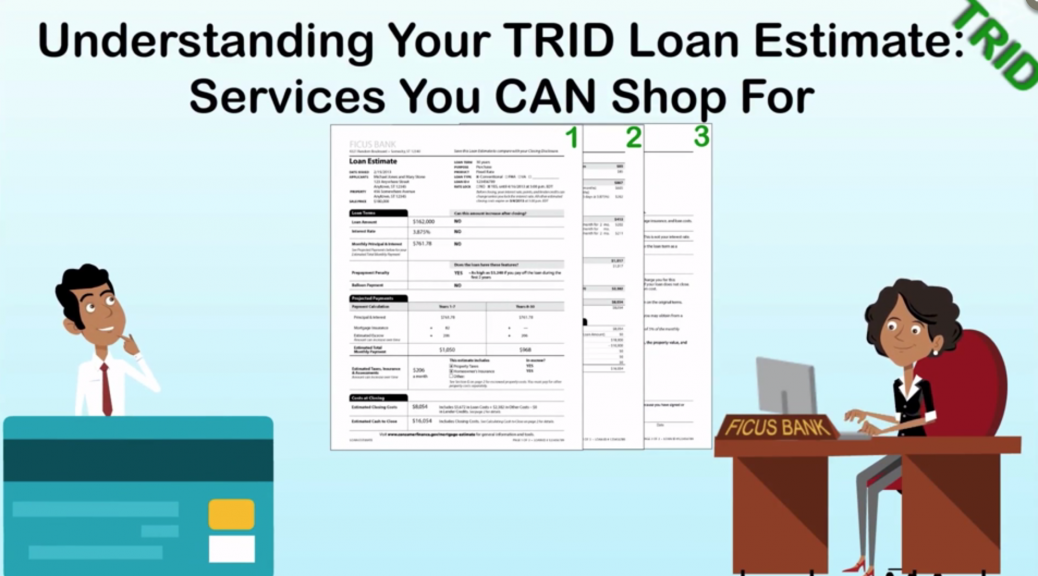

These costs are paid to outside parties and YOU are free to shop and compare providers for a variety of services. These might include pest inspection, or a survey to verify property lines or a range of Title-related services.

Title services might include:

- a Lender’s title policy, which protects their legal interest in their loan collateral- usually the property itself

- settlement agent fees, paid to the individual or company responsible for facilitating the final transaction

- Title Search, which clarifies and documents legal ownership of the property

- a title insurance binder, which allows potential future use of the current title search results, conditions and exclusions for a short period to lower the cost of future title insurance.

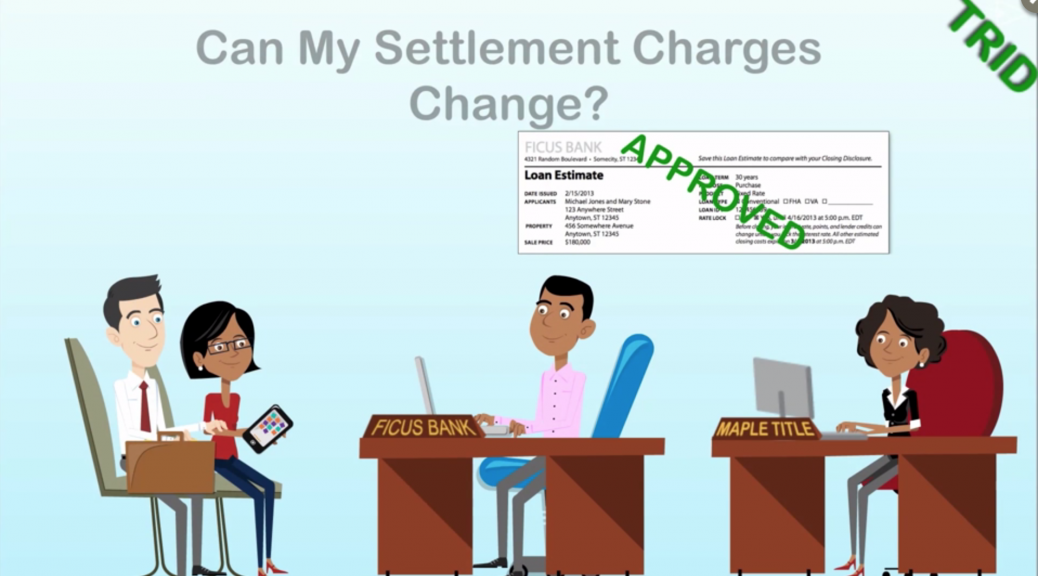

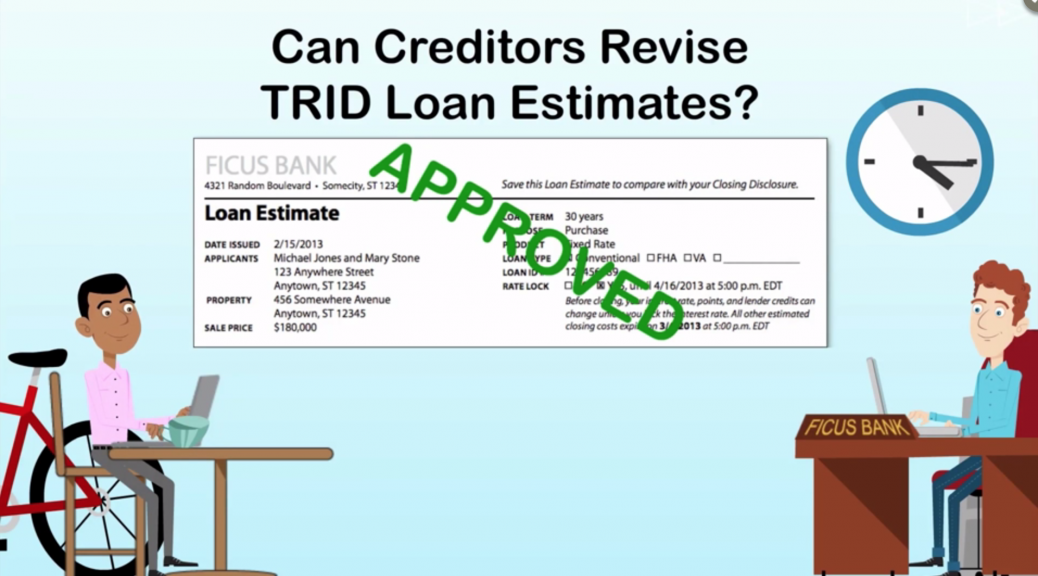

If you select service providers from the list provided by the lender, their fees cannot change by more than 10% between the Loan Estimate and the final Loan Disclosure. If you select other providers the lender is not responsible for changes in those costs.