http://fwd5.wistia.com/medias/49we28kmt9?embedType=iframe&videoFoam=true&videoWidth=640

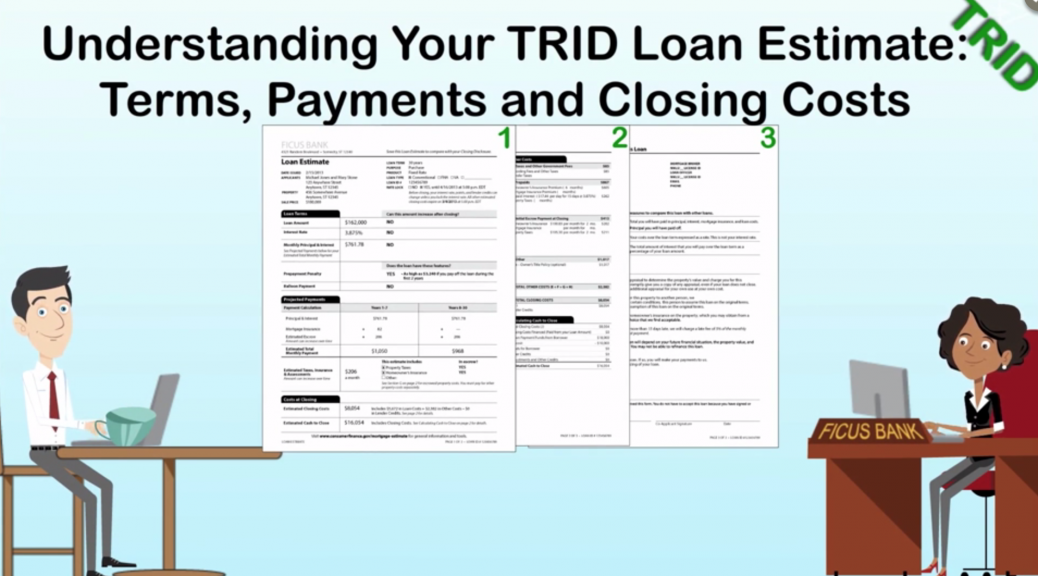

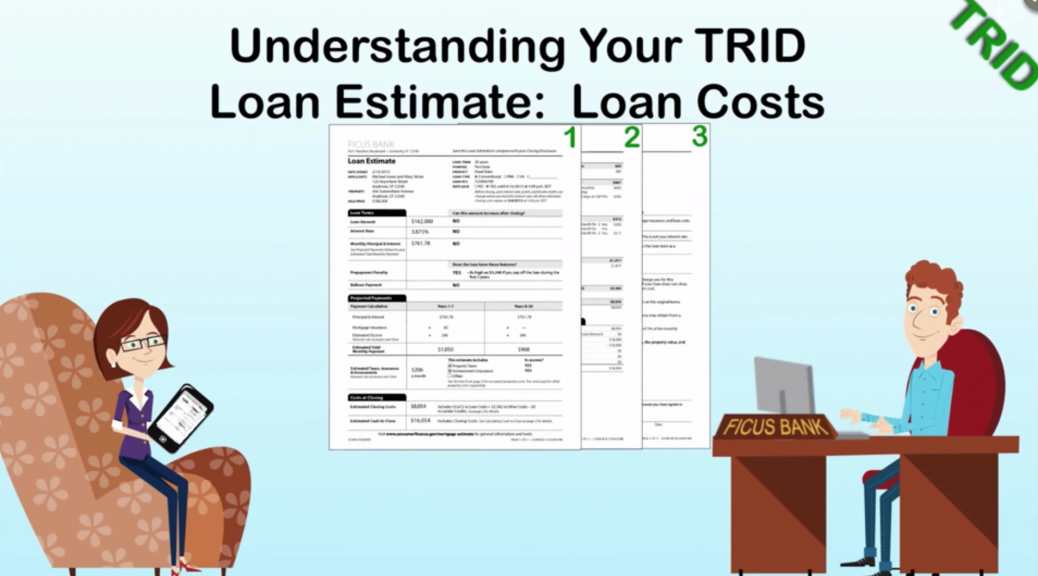

Closing costs are fees paid when the title of the property is transferred to the buyer making them the legal owner.

Origination Charges are fees collected by the lender for the loan process. They may including fees for handling the loan application and “Origination Fees”, which are compensation paid by the creditor to the entity that originated your loan.

“Points” are fees paid to lower interest rates; points are considered prepaid interest for the buyer, and are usually tax deductible.

Finally, Underwriting is a payment to the lender for their assessing the risk that the loan might not be repaid, based on the loan specifics and your financial characteristics.