http://fwd5.wistia.com/medias/welthz1jzx?embedType=iframe&videoFoam=true&videoWidth=640

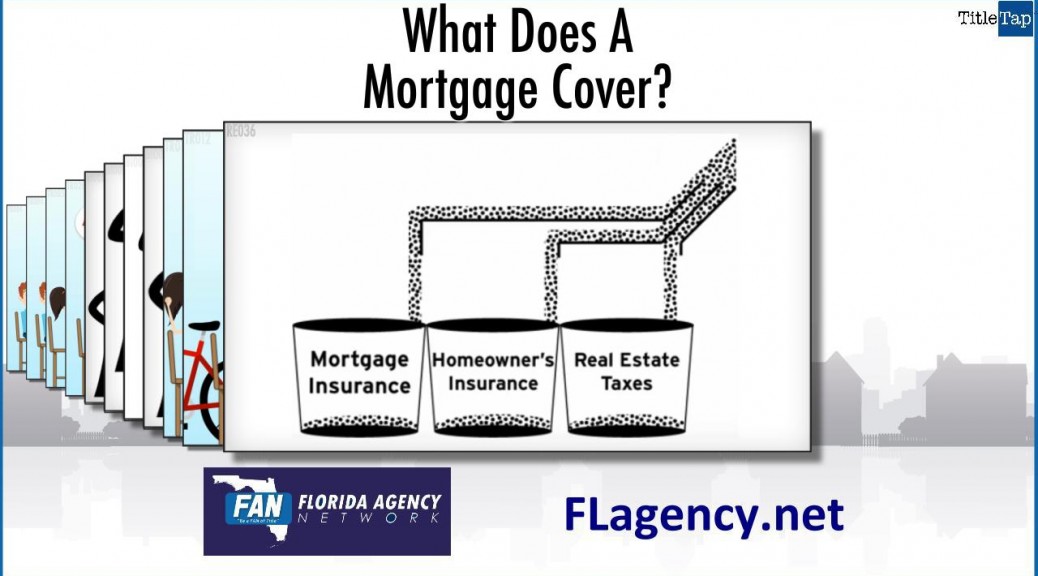

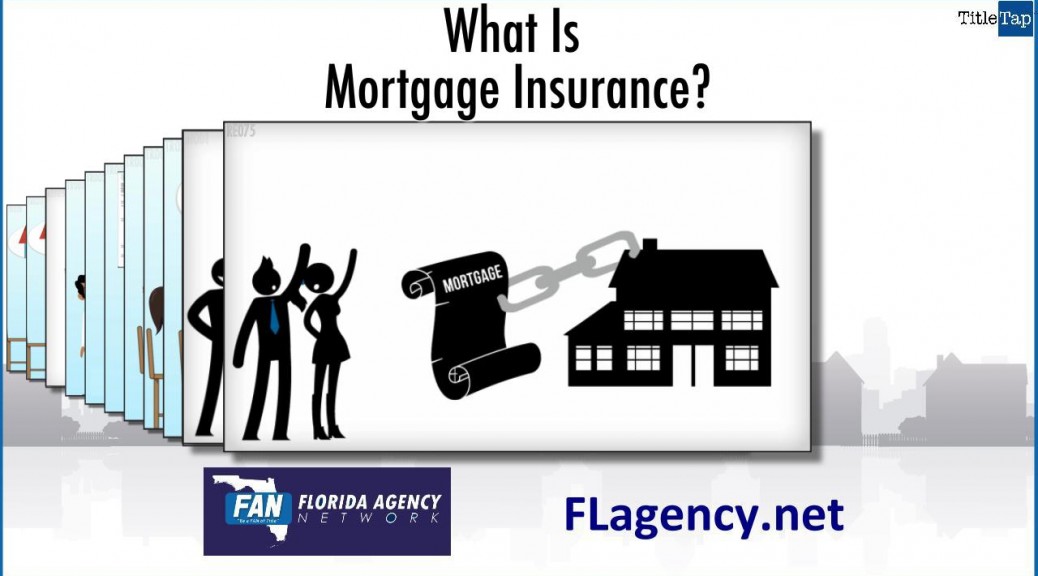

Like the video shows, mortgage insurance is a policy that protects lenders against some or most of the losses that result from defaults on home mortgages. Like home or auto insurance, mortgage insurance requires payment of a premium, is for protection against loss, and is used in the event of an emergency.

If a borrower can’t repay an insured mortgage loan as agreed, the lender may foreclose on the property and file a claim with the mortgage insurer for some or most of the total losses.

You generally need mortgage insurance only if you plan to make a down payment of less than 20% of the purchase price of the home. The FHA offers several loan programs that may meet your needs.