http://fwd5.wistia.com/medias/0k5k9nuvuy?embedType=iframe&videoFoam=true&videoWidth=640

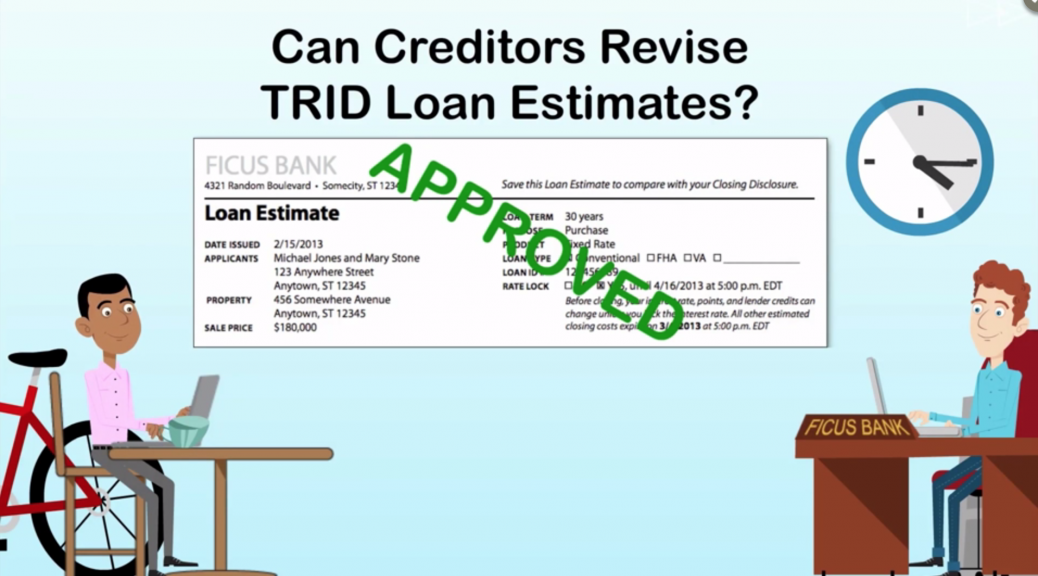

Creditors are generally bound by the initial Loan Estimate. They are permitted to provide a revised Loan Estimate only under certain changed circumstances. These include circumstances that:

a) increase settlement charges beyond the legal tolerance limits

b) affect YOUR eligibility or change the value of the loan security.

Also,

c) if the interest rate was NOT locked and the new rate changes points or lender credits

d) for settlement delay on new construction loans within the stated revision window – typically 60 days, or

e) if YOU indicate an intent to proceed more than 10 business days after the Estimate or request loan term revisions.

Changed circumstances are extraordinary events beyond the control of you or the lending parties, OR changes or inaccuracies revealed in the information the lender used in preparing the Loan Estimate, OR new information on you or the transaction that the creditor did not use in the Loan Estimate.